US and International Equities

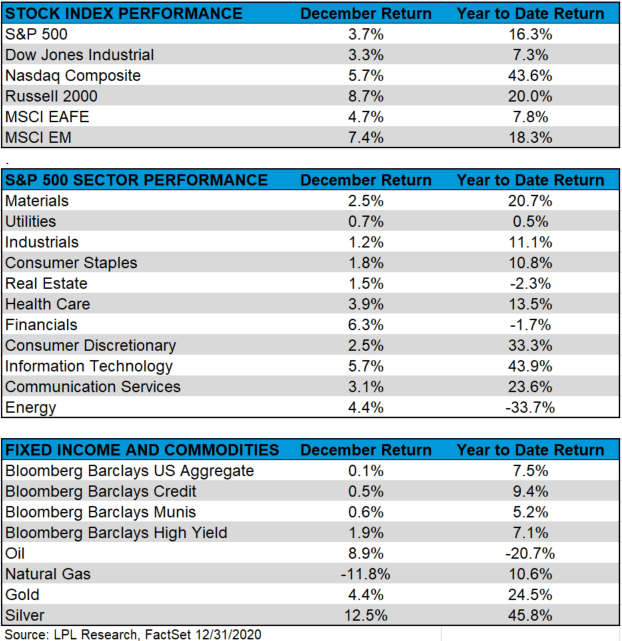

The S&P 500 Index, Dow Jones Industrial, and Nasdaq Composite indexes, continued their November run in December. As noted last month, November was a record-breaking month for equities, thanks to positive vaccine news, a strong third quarter earnings season, and a likely split Congress. Even in the wake of weak economic data, market participants are looking forward to a new year and a potentially better economic landscape.

Information Technology Sprints Ahead While Financials Rebound

Financials were the best performing sector for December. The sector had been challenged for much of the year by the rate environment as well as the potential for more commercial and consumer loan defaults. Improved recent performance has been supported by an improved timeline for an economic recovery and a steepening yield curve (the difference between long-term and short-term rates).

Technology also had a solid December, continuing its dominance this year, returning over 43% year to date. This sector has benefitted from COVID-19-related demand for products and services such as remote learning, meetings, and entertainment.

Energy returned over 4% in December, following up on its strong run in November. The sector has been a major detractor to S&P 500 performance this year and finished down over 30% year to date.

Utilities Power Back

After two straight positive months in September and October—the only sector to accomplish that feat—utilities earned a marginally positive return and ended both December and November as the worst performing sector.

International Market Resilience

Like their domestic counterparts, international equities finished the month solidly higher. Emerging markets stocks, measured by the MSCI Emerging Markets (EM) Index, outperformed developed market equities, as indicated by the MSCI EAFE Index. Nevertheless both indexes returned over 4.5% for December.

Small Cap Strength

As we have noted during previous Weekly Market Performance blogs, small cap stocks have been standout performers recently. The small cap Russell 2000 Index outperformed all the major market US and overseas indexes for December. For more of our thoughts on small caps, please read Weekly Market Commentary: Three Reasons We Like Small Caps.

Fixed Income, Currencies, and Commodities

The bellwether Bloomberg Barclays US Aggregate Index finished the month fractionally higher. Major bond sectors mirrored the broad index’s performance in lockstep. High yield bonds, designated by the Bloomberg Barclays High Yield Index, finished the month a little less than 2% higher. International bonds, denoted by the FTSE World Government Bond Index, and emerging markets debt, measured by the JP Morgan Emerging Markets Bond Index (EMBI), also ended the month higher.

Commodities were solid performers with the exception of natural gas. Natural gas has experienced much volatility during the fourth quarter of 2020. The commodity finished 32.8% higher in October, fell 14.1% in November, and gave back an additional 12% in December. Copper finished the month in the green gaining over 1%. Gold and silver ended higher to close out December with silver the standout, returning over 12%.

US and International Economic Data Recap

Conference Board’s Leading Economic Index (LEI). The Conference Board’s Leading Economic Index (LEI) increased 0.6% month over month in November. This follows a 0.8% increase in October along with 0.7% increase in September. The growth in the November LEI fell to its slowest pace in five months. New orders for manufacturing, average weekly initial claims for unemployment insurance, residential construction permits, along with equity prices were the strongest positive contributors to November’s LEI. Declining manufacturing working hours along with consumers’ outlook for the economy weighed on the index.

Inflation. Inflationary pressure remained tame in November, with the core Consumer Price Index rising 1.6% year over year, increasing fractionally on a month-over-month basis. Producer prices, measured by the core Producer Price Index, increased just under 1% year over year. This was less than expected and shows that producers are having marginal success increasing prices as the economy tries to recover from the impact of COVID-19. Inflation has risen slowly from low levels, but may still reach the Federal Reserve’s (Fed) inflation target by mid-year, at least temporarily, as the early impact of COVID-19 rolls off the year-over-year numbers.

US Consumer. The Conference Board’s Consumer Confidence Index fell in December from November’s reading, missing analysts’ consensus, and currently remains well below the pre-COVID-19 report from February 2020. The Present Situations Index declined sharply whereas the Expectations Index increased, reflecting the near-term impact of the surge in COVID-19 cases, but the improved longer-term prospects from more widespread vaccine distribution. In addition, US holiday sales increased over 2% from November to December 24th. This increase was less than what market participants expected and mirrors the near-term concerns in the consumer confidence data.

US Home Sales. Sales of previously owned US homes declined last month for the first time in six months. This may signal that surging prices and a low supply could be curbing demand. Median selling prices have risen over 14% year over year, potentially pricing some buyers out of the market. For more of our thought on housing prices, please read the LPL Research Blog, Housing Data Continues to Surge. This increase in home sales should help spending on home amenities as well, something that will be watched by market analysts.

US Business. The National Federation of Independent Business (NFIB) Small Business Optimism Index declined in November by over 2 points but was still above average. Moreover, the NFIB noted that the November’s uncertainty reading declined as well. Given the current COVID-19 climate, small business owners are dealing with major uncertainties, especially amid increased restrictions at both the state and local levels.

Federal Reserve Open Market Committee (FOMC). Following its December meeting, the FOMC, the Federal Reserve’s (Fed) policy arm, announced asset purchases would continue at their current pace and the Fed’s policy rate would remain at a target range of 0–0.25% but sharpened its guidance on how long it would continue its bond purchase program, also known as quantitative easing (QE). Fed Chairman Powell also noted that the Fed has the ability to buy longer-maturity bonds in the future, as some market participants have desired, to further help the economic recovery.

US Employment Claims. The US unemployment rate still remains high compared to history. COVID-19 continues to play an adverse role on service industry employment in particular. Even though the unemployment rate has declined from a peak of approximately 15%, we are quite far from having an economy at full employment. The distribution of a COVID-19 vaccine should help the employment landscape.

Looking Ahead

Investors will be following the run-off elections for the two Georgia senate seats this week. The result will determine which party controls the US Senate and whether there will be split-party rule.

Even with much positive news on the COVID-19 vaccine front, COVID-19 number spikes are still weighing on investors’ minds. As is evident from the economic reports, the effects of government restrictions on economic growth will also be closely watched by market participants, although the emphasis will remain forward looking. How we manage COVID-19 in the wake of ramped-up vaccine production and distribution will have a major influence on the investment landscape in 2021.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. All market and index data comes from FactSet and MarketWatch.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

For a list of descriptions of the indexes referenced in this publication, please visit our website at lplresearch.com/definitions.

This Research material was prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking 1-05094700